Editor’s note: The markets are closed for Presidents' Day. So we’re bringing in our friend, 40-year market veteran and highly respected financial educator Keith Fitz-Gerald, to share some timeless wisdom that can dramatically improve your investing results.

Read on to see Keith’s 3 specific “maxims”...

And if you haven’t yet watched his recent interview, in which he covers how to navigate today’s markets and much more, it’s still available at this link.

***

Today’s essay is what my grandmother Mimi would call a teaching moment.

Let’s start with a tweet I posted recently, then we’ll talk about how that translates into current market action. Then we’ll have a chat about why this matters... and how you can use that information to immediately improve your results.

First, the tweet…

It’s tough love, to be sure.

Here’s the thing.

Aspiring investors are often more concerned about being right than they are about being profitable. Successful investors, on the other hand, know that it’s possible to be profitable even if they’re dead wrong when it comes to market expectations.

Social scientists say this is because we’re wired that way. They chalk it up to the desire to be “more right” than somebody else and consider it a part of the human condition.

In some cases, that’s driven by the anxiety of abandonment because they want to be aligned with the “right” way of thinking about this or that issue within a group of peers. This is why social media is so dangerous, especially lately.

Avoiding disappointment is a biggie, too. People, particularly aspiring investors, tend to choose actions and make decisions based on what lines up with their expectations. So they favour the expected, as opposed to the likely or the unexpected—which, when you think about it, is how you make the big bucks.

There’s also the fear of failure, especially with the financial markets. People fear the consequences of being wrong more than they relish the rewards of being profitable. So they’d rather stick to the same tired old tactics that haven’t worked for a decade instead of seeking fresh counsel and changing up their tactics.

The death of the 60/40 portfolio is a particularly graphic example of something that’s broken down recently. Diversification is another.

Here’s why you should care.

Counterintuitively, the need to be right is a performance limiter. You’d think that wouldn’t be the case, but it is.

Take buying stocks, for example.

There are more than 600,000 securities listed worldwide. Every stock screener I’ve ever seen is designed to help you slice and dice the information needed to research ‘em a bazillion ways from Sunday. The average investor has so many choices that they’re simply overwhelmed or left exhausted.

One even said to me recently, “I’d rather go to the dentist and have a tooth pulled!”

It’s no wonder that people give up or are left with more questions than answers.

A 2004 study on behavioural finance published in Pension Design and Structure: New Lessons in Behavioral Finance found that people faced with more choices actually saved less for retirement.

I agree.

People want all the choice in the world because they think it’s empowering when, in fact, the opposite is true… too much information results in decision paralysis, exhaustion, and a decline in results.

Put another way and in plain English, the more options there are, the less likely you are to achieve the results you want and the profits you deserve.

Fixing this problem isn’t particularly challenging.

In fact, doing so comes down to three specific maxims.

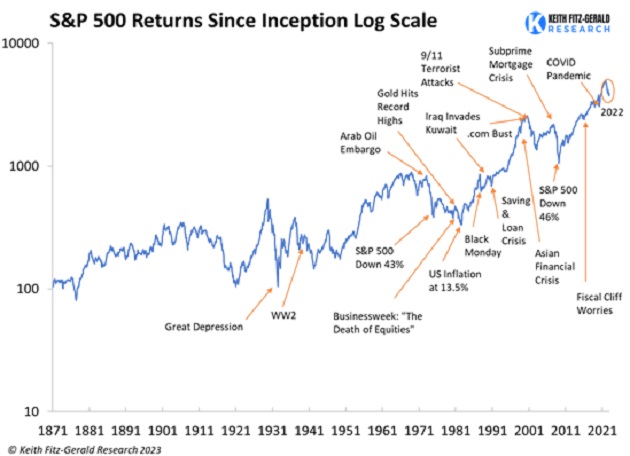

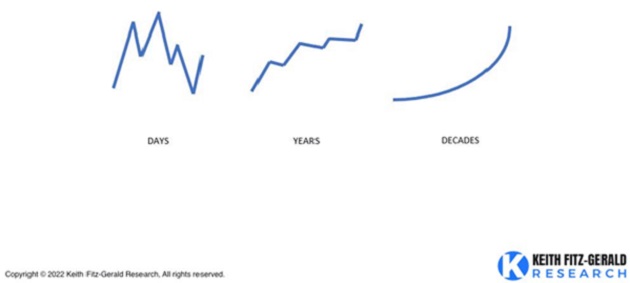

Maxim #1: The markets have an upside bias.

People constantly worry about the markets at moments in time when the daunting reality is that learning to invest over time is the key. Tactics are how you control risk along the way.

Wall Street’s marketing geniuses have spent billions of dollars learning how to push your buttons by getting you to focus on the short-term news cycle... even as they separate you from long-term wealth that would otherwise be in your pocket.

They are well versed in the behavioural biases I’ve just shared with you, which is why they ply their trade the way they do. Wall Street knows that retail investors are more likely to make emotionally driven decisions under duress—and that you’ll trade more often when that’s the case.

That’s why learning to “zoom out” can be a huge advantage!

No doubt you see what I mean.

Maxim #2: Buy the best, ignore the rest.

People delude themselves into thinking they’ve got to find the next great undiscovered stock. That worked once upon a time, but the world we live in now means that the big money concentrates almost exclusively on the world’s best companies as a function of liquidity.

Computerization, Dark Pools, and the rise of passive investing have changed the game forever.

My research, for example, shows that there are only about 50 stocks that matter at any given time out of more than 600,000 listed securities worldwide. That’s why I go to extraordinary lengths to identify ‘em in my paid research magazine, One Bar Ahead®.

This isn’t rocket science… but it is behavioural science!

And the sooner you make friends with that idea, the sooner you can get down to business.

Maxim #3: Always do what Wall Street does, not what it says.

Wall Street analysts have a long, less-than-stellar record of saying one thing and doing another. It’s an open secret that “the Street” trades against clients who are following the same advice they’re busy avoiding. Or worse, that investment bankers and other insiders simply tip off clients to looming sales.

Sell-side analysts were busy telling you, for example, that Meta was a great buy at $350 and that Robinhood would be an unprecedented opportunity.

My take was different.

I called the former a bug in search of a windshield and “would fall to less than $100” and said that the latter would be the “biggest self pump and dump in history” the day it listed.

Research from Barron’s, DALBAR, and others shows that investors routinely buy when they should be selling and sell when they should be buying.

Again, I agree.

Warren Buffett says to “be greedy when others are fearful.”

The late Sir John Templeton said to “buy when others are despondently selling.”

My take is that “chaos creates opportunity.”

If you’re scared and uncertain, I get it. We live in a complicated world at a challenging time in history.

Just remember that the weak money inevitably gets shaken out at the bottom of every major market move at a time when the big money players have been waiting for them to throw in the towel.

Great companies like Apple, Tesla, and others we talk about frequently are not likely to disappear anytime soon. They will power through this mess and return to new highs faster than most people are prepared to accept.

The bottom line is very simple.

You can learn to embrace the uncertainty others fear or get carried out feet first by those who do.

You got this—I promise!

Now, and as always, let’s MAKE it a profitable day!

Keith

***

Editor’s note: For more Keith, make sure to watch his recent interview. You’ll discover:

- Keith's investing framework, including the tools he uses to weigh one opportunity vs. another.

- The reason why, among 600,000+ tradable securities worldwide, only 50 truly matter for most portfolios.

- Keith's thoughts on Apple, Tesla, Microsoft, Peloton, Goldman Sachs, defense tech names… cybersecurity… AI… and more.

- How to improve your "mental game" when making portfolio decisions.

- And much, much more.